For no good reason outside of my own curiosity I have taken on a project of analyzing what shows up in my mailbox. After eleven weeks of collecting information, there are some interesting things that I’ve observed. How useful this project is, or will be, remains questionable. But I can find no signs online of anyone doing this sort of project, so perhaps it will reveal something valuable. Even with eleven weeks of data, the numbers are still relatively small, so we should be careful not to draw any concrete conclusions just yet.

First, let’s start by looking at what has shown up in the mailbox each week. As much as some folks rant against stacked bar charts, I think they can be useful in some situations. Situations like this, for example. Here we can see the weekly volume of mail that my local carrier delivered to the box, how that number changed over time, and what the majority category was for each week. Each week’s bar is sorted by quantity, with the largest quantity category placed at the bottom. This makes large changes easy to spot. It should be easy, for example, to grasp when the last election took place from the sudden rise (and subsequent disappearance) in the purple bars.

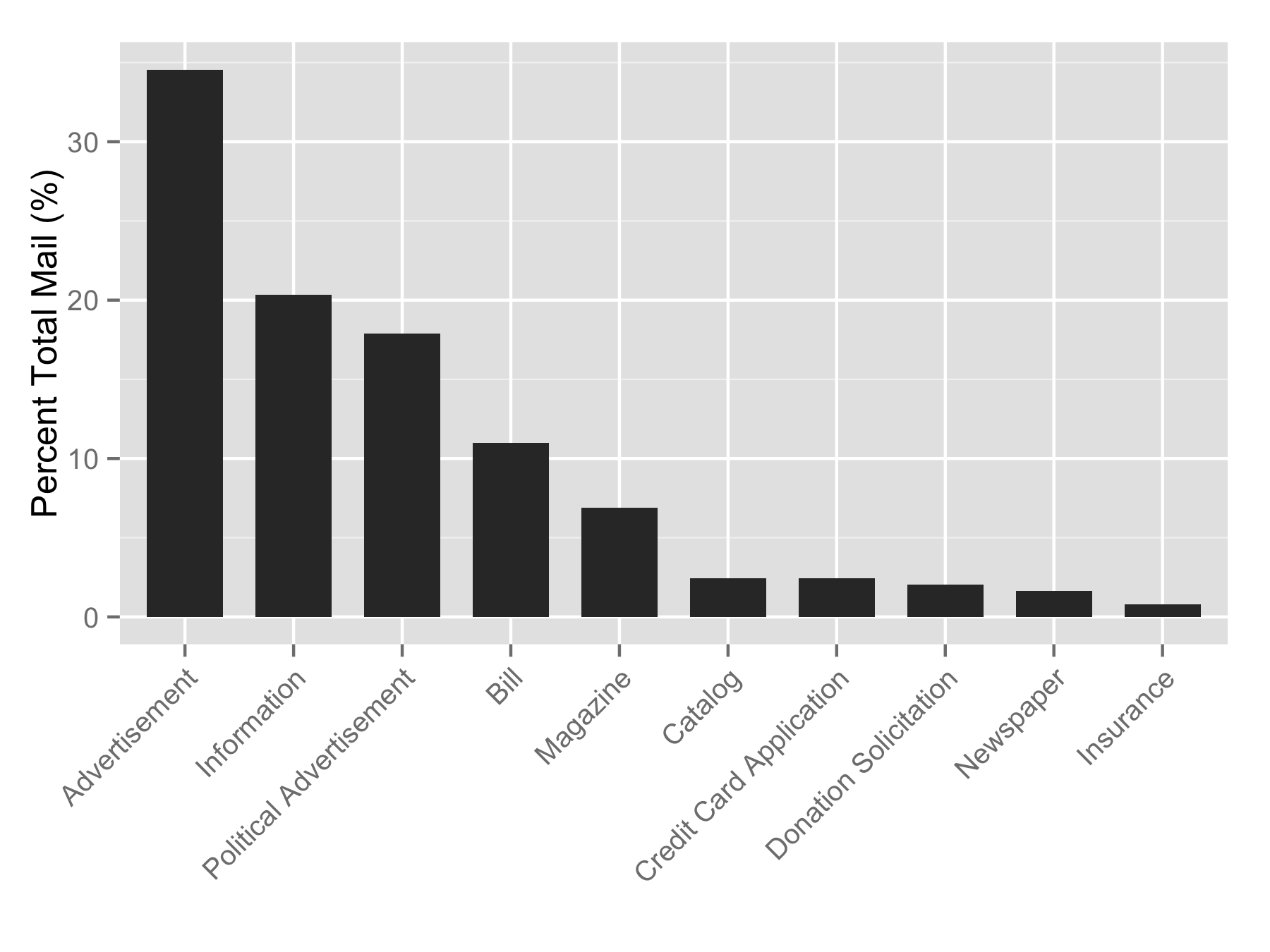

Eleven weeks of USPS mail, by category.

In brief, over these eleven weeks I received anywhere from 13 to 33 pieces of mail each week. The average was 22 pieces of weekly mail with a standard deviation of about 6.5. I’m not sure that a Gaussian model is the right one for this type of data (Poisson is probably more reasonable), but it gives a reasonable summary for a smallish data set. Examining the distribution statistics is something I intend to do once the dataset grows a bit larger.

The relative breakdown between the categories is not surprising. Advertisements dominate the composition. I trust the political ads will be competitive for second place as the November election gets closer. What I think this shows pretty clearly is how the Post Office gets paid. Fully half of the mail I have received has been advertising, either the normal (34.5%) or the political flavor (17.8%). I don’t think I would have guessed it to be that high. If there is ever legislation passed to limit junk mail, the USPS will be in bigger financial trouble than they’re in already.

What I find terribly interesting, though, is the breakdown by weekday. Meaning, the day of the week that the piece of mail was received. Eleven weeks is not the biggest sample size, and so this may not hold true in the long run. But Friday is absolutely a dominant day for the quantity of mail. And not just for a single category. The three major categories all have big mail days on Friday.

Mail totals by day of the week.

We can see this more clearly by looking at the categories separately. I’ve separated out the weekly totals in actual pieces of mail for these categories. First are “Advertisements,” otherwise known as “junk mail.” Friday stands above the crowd with 22 above Wednesday’s 19. Monday, Tuesday, and Saturday all come in at 10, so this difference appears to be significant.

Then we have “Information.” This is mail from people or businesses that I have a relationship with. Doctors’ offices, schools, banks, etc. This is a very big Friday category with 18. The next largest day is Saturday with 9.

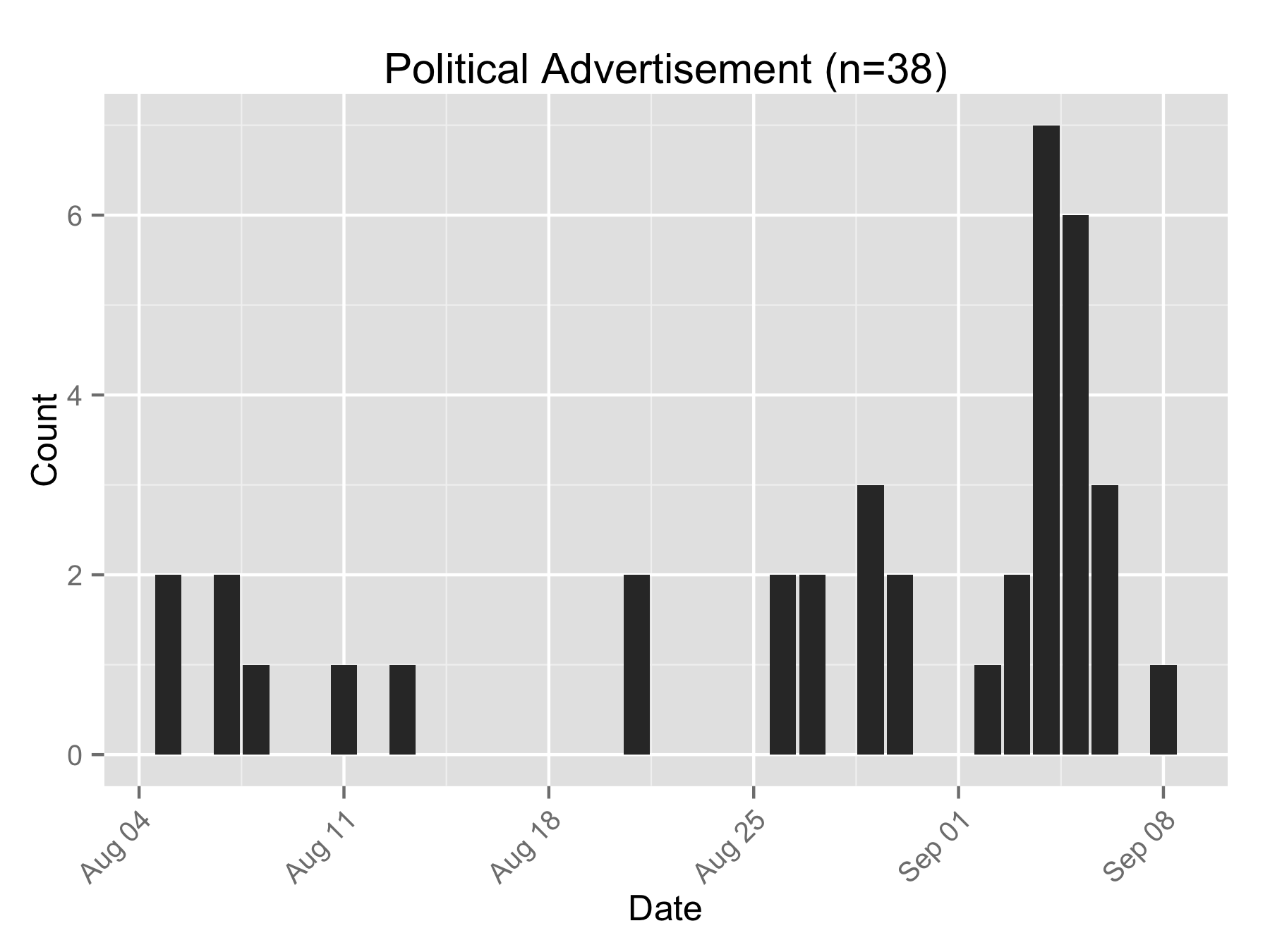

And then “Political Advertisements.” I’m somewhat conflicted on how valid this category is. There was an election held on a Tuesday, and the direct mail spike happened on the Thursday (7 pieces) and Friday (6 pieces) of the week before. Since the election I have received at most one political advertisement on any given day. So this contributes to the “big Friday” effect, to be sure, but it was just one week out of eleven, so its impact is mitigated by its relative rarity. But note that eliminating the category altogether would still result in Friday being the dominant weekday for mail delivery.

So this “big Friday” effect seems like it might be real. But the raw numbers are still relatively small and the time relatively short. So I’m cautious about drawing too many conclusions just yet, but it certainly is an interesting, if preliminary, result.